Forecasting gold volatility with geopolitical risk indices |

| |

| Affiliation: | 1. School of Economics and Management, Southwest Jiaotong University, Chengdu, China;2. School of Economics, Qingdao University, Qingdao, Shandong, China;3. Adnan Kassar School of Business, Lebanese American University, Beirut, Lebanon |

| |

| Abstract: |

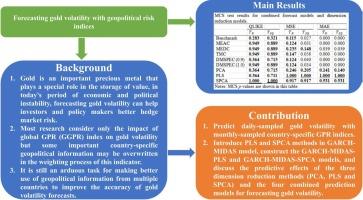

This paper tries to forecast gold volatility with multiple country-specific (GPR) indices and compares the role of combined prediction models and dimension reduction methods regarding the improvement of gold volatility prediction accuracy. For this purpose, GARCH-MIDAS model’s several extensions are used. We find firstly that most country-specific GPR indices have driving effects on gold volatility, and it makes sense to take forecast information from multiple country-specific GPR indices into account when forecasting gold volatility. The out-of-sample empirical results also indicate that the dimension reduction methods yield better predictions compared to the combined prediction models. In addition, dimension reduction technologies have excellent forecasting performance mainly during low gold volatility periods. Finally, our empirical findings are robust after changing the evaluation method, model settings, in-sample length and gold market. |

| |

| Keywords: | Gold Volatility Combined Prediction Dimension Reduction Geopolitical Risk |

| 本文献已被 ScienceDirect 等数据库收录! |

|